Quick Answer, Best Futures Contracts to Trade

- NQ (E-mini Nasdaq 100) is the best day trading futures contract for most active traders: wide daily range, strong trends, $5/tick.

- MES and MNQ are the right starting point for beginners, prop firm evaluations on smaller accounts, and strategy testing.

- ES (E-mini S&P 500) is the most liquid contract in existence, ideal for scalpers who need one-tick spreads at size.

- CL (Crude Oil) offers the highest per-session range in dollar terms but carries serious overnight gap risk.

- Prop firms universally allow ES, NQ, MES, MNQ. CL, GC, and bond futures get restricted at roughly half of firms.

---

What Makes a Futures Contract Worth Trading?

Four things matter: liquidity, daily range, tick value relative to your drawdown, and spreads.

Liquidity means you can exit a bad trade without paying a spread penalty. ES and NQ both have this. CL has it during US hours. Outside of the US session, CL's order book thins. Agricultural contracts like Wheat (ZW) or Natural Gas (NG) can have gaps in the book that cost you a tick just on the fill.

Daily range sets your profit ceiling per session. A contract that moves 10 points gives you more to work with than one that moves 3. The catch is that wider range also means a larger adverse move if you're on the wrong side.

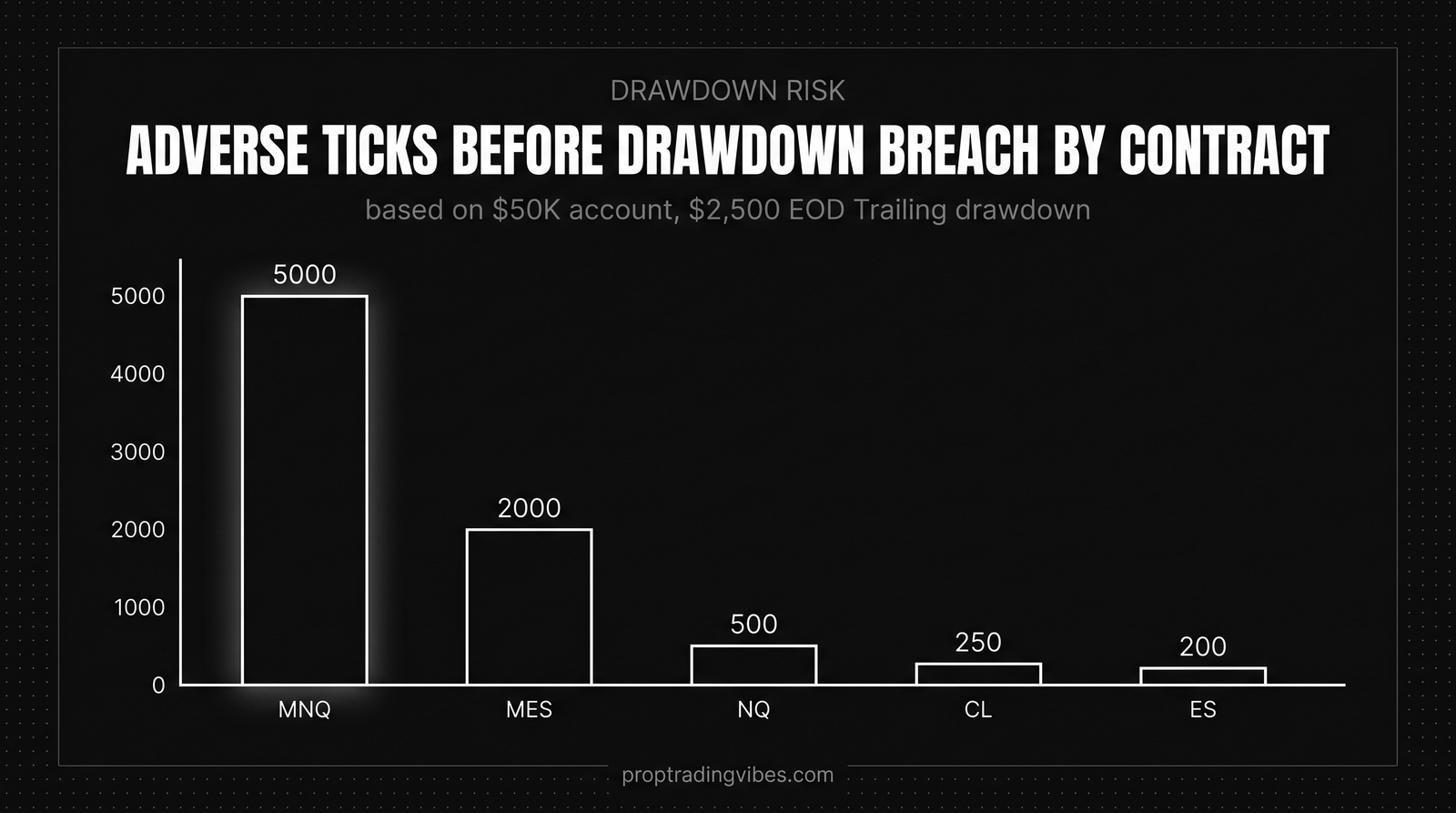

Tick value vs. drawdown is the calculation most traders skip. Take your max trailing drawdown, divide by the tick value, and you get the number of adverse ticks you can survive on one contract. On a $50K prop account with a $2,500 EOD Trailing drawdown limit:

| Contract | Tick Value | Adverse Ticks Before Drawdown Breach |

|---|---|---|

| MES | $1.25 | 2,000 ticks |

| MNQ | $0.50 | 5,000 ticks |

| ES | $12.50 | 200 ticks |

| NQ | $5.00 | 500 ticks |

| CL | $10.00 | 250 ticks |

That table doesn't lie. MNQ gives you 10x the room that ES does on the same account.

Spreads on the major equity index futures are one tick during Regular Trading Hours. Outside US hours or on less popular contracts, spreads widen fast.

---

Full Ranking: Best Futures Contracts for Prop Firm Traders

Rankings here weight drawdown compatibility, prop firm access, and practical profitability in that order.

1. E-mini Nasdaq 100 (NQ)

The contract I trade every day. NQ tracks the Nasdaq 100: heavy on Apple, Microsoft, Nvidia, Meta, Amazon.

| Spec | Value |

|---|---|

| Tick value | $5.00 per tick (0.25 point) |

| Point value | $20.00 |

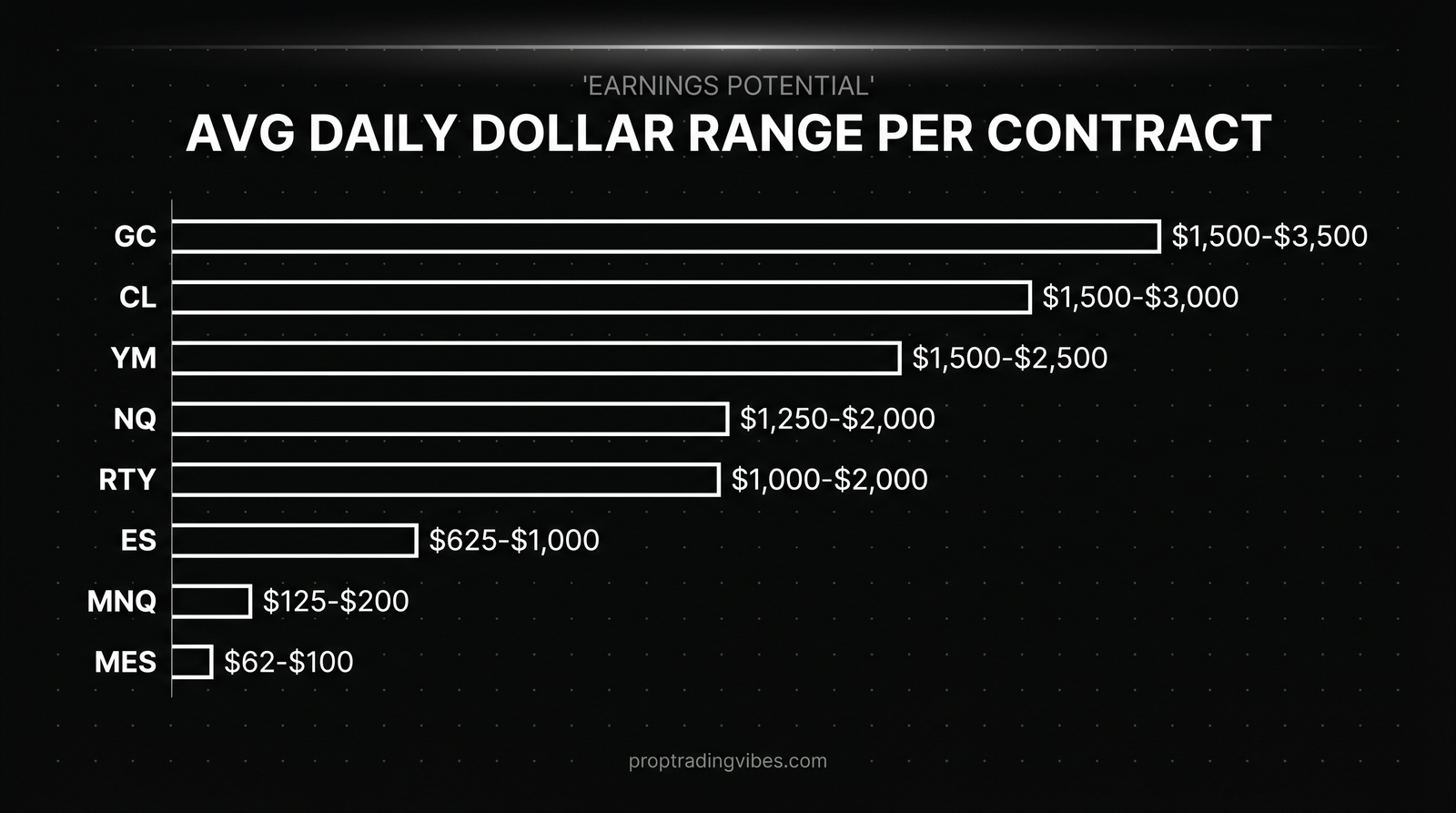

| Typical daily range | 250-400 points |

| Avg daily volume | ~850,000 contracts |

| Day trade margin | $1,000-$2,000 |

NQ trends. On a strong trend day it can run 300+ points in one direction with barely a meaningful pullback. Right side: $6,000+ per contract. Wrong side: your drawdown is gone.

The $5/tick value hits a sweet spot for $50K-$150K prop accounts. It's large enough to generate real money on 1-2 contracts, small enough that a 30-50 point stop doesn't vaporize your buffer.

Every prop firm I've tested allows NQ without restriction: Lucid Trading, Top One Futures, FundingPips, Apex Trader Funding, MyFundedFutures, and the rest. No exceptions in my experience.

2. E-mini S&P 500 (ES)

The most liquid futures contract on the planet.

| Spec | Value |

|---|---|

| Tick value | $12.50 per tick (0.25 point) |

| Point value | $50.00 |

| Typical daily range | 50-80 points |

| Avg daily volume | ~1.5 million contracts |

| Day trade margin | $500-$1,200 |

One-tick spreads. Deep book at all times. You can trade 5-10 contracts without moving the market.

The thing traders get wrong about ES: "it's safer than NQ because the range is smaller." At $12.50/tick versus NQ's $5/tick, that math closes fast. A 10-point adverse move on ES costs $500. On NQ, a 10-point move costs $200. ES's smaller range doesn't make it cheaper per dollar-of-exposure.

ES is the scalper's contract. 2-4 point moves in and out, all day, minimal slippage, one-tick fills. For swing-style prop firm traders, the higher tick value bites harder than most people expect.

3. Micro E-mini Nasdaq 100 (MNQ)

NQ at one-tenth the size. Same chart, same trends, same price action.

| Spec | Value |

|---|---|

| Tick value | $0.50 per tick |

| Point value | $2.00 |

| Typical daily range | 250-400 points |

| Avg daily volume | ~1.2 million contracts |

| Day trade margin | $100-$200 |

On a $25K prop account, MNQ is the smart choice. You can run 3-5 contracts, get real Nasdaq exposure, and survive a bad day without wiping the drawdown buffer. Fills during RTH (Regular Trading Hours) are clean. Spreads widen to 2-3 ticks overnight, so keep that in mind for overnight positions and swing holds.

For anyone new to prop firm evaluations: start here, not on NQ. The MNQ gives you the exact same experience at one-tenth the cost of getting it wrong.

4. Micro E-mini S&P 500 (MES)

The single most-traded micro futures contract. Volume consistently tops 2 million contracts daily, more than most full-size contracts.

| Spec | Value |

|---|---|

| Tick value | $1.25 per tick |

| Point value | $5.00 |

| Typical daily range | 50-80 points |

| Avg daily volume | ~2 million contracts |

| Day trade margin | $50-$100 |

A 10-point adverse move costs $50 per MES contract. You can absorb 10 bad stop-outs before losing what one bad ES trade costs. That's tuition at a price that doesn't end your account.

I don't trade MES regularly because the per-contract profit is too thin for my style. For someone building consistency before scaling, it's the right tool.

5. Crude Oil (CL)

The highest average daily range in dollar terms of any liquid futures contract.

| Spec | Value |

|---|---|

| Tick value | $10.00 per tick (0.01 point) |

| Point value | $1,000.00 |

| Typical daily range | $1.50-$3.00 (150-300 ticks) |

| Avg daily volume | ~700,000 contracts |

| Day trade margin | $2,000-$5,000 |

Wednesday inventory reports and OPEC announcements can move CL $2-3 in minutes. That's $2,000-$3,000 per contract in under ten minutes. The upside is real.

So is the overnight gap risk. CL responds to geopolitical events, inventory data, and energy-ministry announcements at all hours. I've woken up to gap opens on CL that blew straight through a stop. On a prop account, a $1.50 overnight gap on CL is $1,500 gone before you can do anything about it.

Several firms restrict CL or cap it at 1-2 contracts regardless of account size. Top One Futures and Bulenox allow CL but apply tighter position limits. Always verify before buying an evaluation.

6. Gold Futures (GC)

Gold hit all-time highs in 2025 and kept running in 2026. That brought a wave of equity index traders into GC.

| Spec | Value |

|---|---|

| Tick value | $10.00 per tick (0.10 point) |

| Point value | $100.00 |

| Typical daily range | $15-$35 (150-350 ticks) |

| Avg daily volume | ~250,000 contracts |

| Day trade margin | $2,500-$6,000 |

Gold trends in smooth sweeping moves when it gets going. It responds to interest rate expectations, dollar direction, and risk-off flows, which means it often runs when equity index futures are choppy. That uncorrelated opportunity is genuinely useful.

The bid-ask spread is 1-2 ticks during regular hours and 3-5 ticks overnight. At $10/tick, a 3-tick spread costs $30 to cross. GC also has higher margin requirements than any equity index future. Most prop firms allow GC but restrict position size on accounts below $100K.

7. E-mini Dow Jones (YM)

YM tracks 30 large-cap stocks. It used to be one of the most popular day trading contracts; it's lost ground to NQ and MES over the last few years.

| Spec | Value |

|---|---|

| Tick value | $5.00 per tick (1 point) |

| Point value | $5.00 |

| Typical daily range | 300-500 points |

| Avg daily volume | ~150,000 contracts |

The $5/tick value is identical to NQ, and the daily range is decent. The problem is volume. At ~150K contracts daily, YM spreads can widen to 2-3 ticks during fast moves. The price action is also choppier than NQ because the Dow is price-weighted: a single stock like Goldman Sachs can distort the whole index on earnings day.

If you like index futures but find NQ too volatile and ES too expensive per tick, YM is a workable middle ground. Go in knowing the fills won't always be as clean.

8. E-mini Russell 2000 (RTY)

The most volatile equity index future by percentage move.

| Spec | Value |

|---|---|

| Tick value | $5.00 per tick (0.10 point) |

| Point value | $50.00 |

| Typical daily range | 20-40 points |

| Avg daily volume | ~200,000 contracts |

Small-cap stocks are more sensitive to rate expectations and economic data surprises. RTY reacts first and hardest when the market is repricing recession risk. The daily dollar range is comparable to ES.

RTY is choppier than NQ to read with technicals. More earnings surprises, more biotech noise, more idiosyncratic moves in the 2,000-stock universe. I rarely see experienced prop traders choose it as their primary contract.

9. Treasury Bond Futures (ZB and ZN)

ZB is the 30-year. ZN is the 10-year note.

| Spec | ZB | ZN |

|---|---|---|

| Tick value | $31.25 | $15.625 |

| Avg daily vol | ~300,000 | ~1.5 million |

| Best for | FOMC/CPI event trades | Macro positioning |

Bond futures are driven almost entirely by Fed policy, CPI, and employment data. Outside of those catalysts, ZB can chop within a 3-tick range for hours. When the catalyst hits, it moves fast.

ZN has significantly better volume than ZB and tighter spreads. If you trade bonds, ZN is the practical choice. Check the firm's rules first: bond futures are restricted at a meaningful chunk of prop firms.

10. Euro FX Futures (6E)

6E tracks the EUR/USD pair on CME. It's the exchange-traded alternative for traders who come from a forex background.

| Spec | Value |

|---|---|

| Tick value | $6.25 per tick |

| Typical daily range | 50-80 ticks |

| Avg daily volume | ~200,000 contracts |

6E tends to trend during the London-New York overlap (8 AM-12 PM ET) and then flatten out. The daily range in dollar terms, $300-$500 on a normal day, requires multiple contracts to generate meaningful profit, which increases commission drag.

FundingPips, which serves traders who move between spot forex and futures, supports 6E. Most other futures-focused prop firms allow it too.

---

Complete Contract Comparison

| Contract | Tick Value | Day Margin | Avg Daily Range | Avg Vol | Prop Firm OK? |

|---|---|---|---|---|---|

| NQ | $5.00 | $1,000-$2,000 | 250-400 pts | ~850K | Yes (all) |

| ES | $12.50 | $500-$1,200 | 50-80 pts | ~1.5M | Yes (all) |

| MNQ | $0.50 | $100-$200 | 250-400 pts | ~1.2M | Yes (all) |

| MES | $1.25 | $50-$100 | 50-80 pts | ~2M | Yes (all) |

| CL | $10.00 | $2,000-$5,000 | $1.50-$3.00 | ~700K | Limited |

| GC | $10.00 | $2,500-$6,000 | $15-$35 | ~250K | Limited |

| YM | $5.00 | $500-$1,000 | 300-500 pts | ~150K | Yes (most) |

| RTY | $5.00 | $500-$1,200 | 20-40 pts | ~200K | Yes (most) |

| ZB | $31.25 | $1,000-$2,500 | 1-2 pts | ~300K | Often restricted |

| ZN | $15.625 | $500-$1,500 | 0.5-1.5 pts | ~1.5M | Often restricted |

| 6E | $6.25 | $500-$1,500 | 50-80 ticks | ~200K | Yes (most) |

---

Which Contracts Are Best for Beginners?

Micro contracts. Full stop.

MES is the safest entry. A 20-tick stop costs $25. You can absorb 10 bad trades on MES for what one bad ES trade costs. That margin of error matters when you're still learning order flow and chart reading.

MNQ is my recommendation for beginners who want more directional movement. The Nasdaq has cleaner trends than the S&P in most market regimes. At $0.50/tick, MNQ is actually cheaper per tick than MES, which confuses people. The difference: MNQ moves more ticks per day, so total dollar exposure ends up similar. Check how trading hours affect micro futures liquidity before you go near overnight sessions.

Stay off CL, GC, and ZB until you're consistently profitable on index futures for 3+ months. The progression that works: 20-30 sessions on MES or MNQ. Once you're hitting your daily target and staying within drawdown, move to ES or NQ. I've watched traders blow three evaluations in a week on CL because they skipped the micros. That's $500+ in eval fees gone for one lesson they could have learned on MNQ for $25.

---

Scalping vs. Swing Trading: Which Contracts Fit Each Style

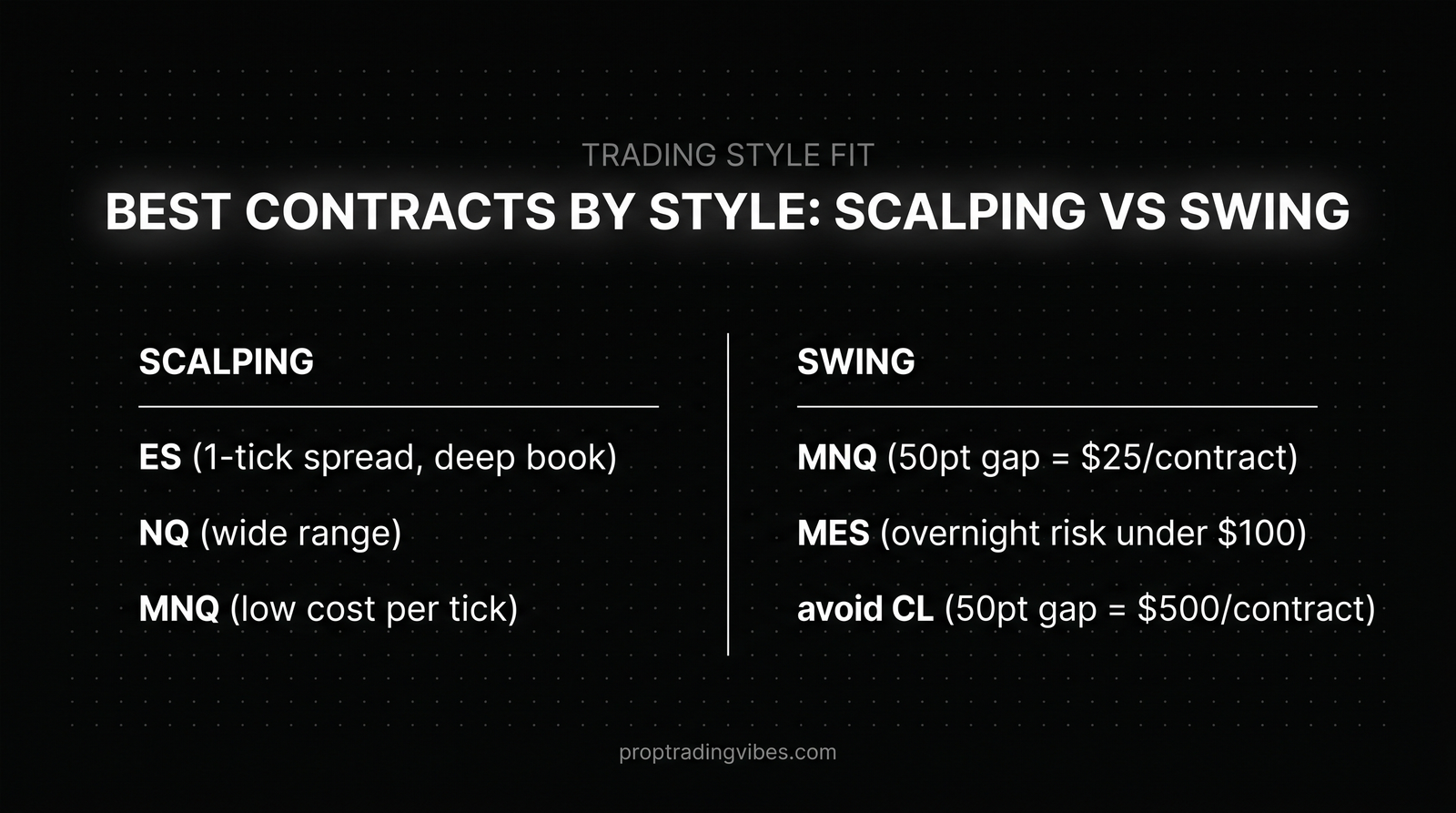

Scalping (seconds to minutes)

ES is the scalper's top pick. One-tick spreads, deep book, 1.5M+ daily volume. You can trade 5-10 contracts without slippage during regular hours.

NQ works for scalping too. My average hold on NQ is 2-8 minutes, targeting 10-20 point moves: $50-$100 per contract. Commissions run about $4.50-$5.50 round-trip per contract, so the math works at a 55%+ win rate.

CL can be scalped but I don't recommend it for most traders. A single tick of slippage on CL costs what two ticks cost on NQ. The $10/tick punishes sloppy entries hard.

Swing Trading (hours to days)

For prop firm accounts with EOD Trailing drawdown, swing contract selection gets tricky. Overnight gaps can eat your buffer before the market even opens.

MNQ and MES are the best swing contracts on prop accounts. An overnight gap that moves 50 NQ points costs $25 per MNQ contract versus $250 per NQ contract. You can hold 5 MNQ through a close and survive a moderate gap.

CL is a poor swing contract on any prop account. Oil gaps routinely on OPEC news and geopolitical events. A single CL contract can move $1,000-$2,000 against you overnight before you can touch the position.

ZB and ZN are actually decent for multi-day holds if you have a clear macro thesis. Interest rate moves tend to be gradual and trending. Most prop firms restrict them though, so verify first. Learn how CME session schedules affect overnight margins before you hold any contract through the close.

---

Contract Selection by Account Size

The math is simple. Max trailing drawdown divided by tick value equals the number of adverse ticks per contract you can survive.

On a $50K prop account with a $2,500 EOD Trailing drawdown:

- NQ ($5/tick): 500 adverse ticks, 125 NQ points. Comfortable for a 30-50 point stop.

- ES ($12.50/tick): 200 adverse ticks, 50 ES points. Workable but tight.

- CL ($10/tick): 250 adverse ticks. Sounds fine until CL moves 100+ ticks in 20 minutes on an inventory report.

- MNQ ($0.50/tick): 5,000 adverse ticks. Massive buffer. Near impossible to blow the drawdown on one MNQ contract.

The rule I follow: never risk more than 30% of remaining drawdown on a single trade. On a $2,500 drawdown trading NQ, that's $750 max per trade, or 150 ticks (37.5 points). That's tight but doable.

On CL, 30% of drawdown is 75 ticks, which gives you $750 of room on a contract that can move that much in a single news spike. The risk-reward math on CL in a prop account doesn't work for most traders.

When in doubt: go smaller. Trading 3 MNQ contracts gives you the same dollar exposure as 0.3 NQ contracts (which you can't actually trade). And you can scale out of MNQ at multiple levels, which matters more than most people realize.

---

Which Contracts Do Prop Firms Restrict?

As of June 2026, the general pattern across the major firms:

Always allowed: ES, NQ, MES, MNQ. I've tested over 20 firms and never seen these four restricted.

Usually allowed with position limits: YM, RTY, CL, GC. On a $50K account that allows 5 NQ contracts, expect a cap of 2 CL or GC contracts.

Often restricted: ZB, ZN, 6E, agricultural futures (ZW, ZC, ZS), natural gas (NG). Bond and currency futures are allowed at roughly half the firms I've tested. Agricultuals and NG are restricted at most.

Micro versions: Almost always allowed even when the full-size is restricted. If a firm blocks CL, they often still allow MCL. Same with GC and MGC.

Lucid Trading has one of the broadest instrument lists. Top One Futures covers all major equity index futures plus CL and GC. TradeDay and Apex Trader Funding are similar in scope. Always verify on the firm's website before purchasing an evaluation, because these lists change.

---

Why I Trade NQ Over Everything Else

I keep coming back to NQ. My reasons are specific to my style.

NQ trends. On most days it picks a direction by 10:00 AM ET and runs with it. The tech-heavy weighting means that when institutional money flows into or out of growth stocks, the move is directional and sustained. I enter on a pullback into the trend and look for 50-100 points. That's $250-$500 per contract on a single trade.

The $5/tick value works for the $50K-$150K prop accounts I mostly trade. Large enough that a good trade generates meaningful profit, small enough that a 40-point stop doesn't consume half my drawdown buffer.

NQ also has personality after you've watched it long enough. The 10:00 AM reversal. The 2:00 PM drift into the close. The pre-FOMC compression followed by a directional break. After two years trading it daily, I read those patterns faster than I do on ES or CL.

I drop to MNQ on days when I'm not confident in the setup. That flexibility, to test a thesis at one-tenth the risk, isn't available on CL or GC in a meaningful way. MCL and MGC exist but the liquidity is thin.

The bottom line: the best futures contract is the one you understand deeply, fits your account size, and aligns with your trading style. For me, that's NQ. For a beginner on a $25K prop account, it's MNQ or MES. For an experienced trader who loves momentum and can handle $10 ticks, CL or GC might be right.

Match the contract to your reality. Get the specs right using this breakdown of available micro futures contracts.

---

Frequently Asked Questions

What is the best futures contract for beginners?

MES (Micro E-mini S&P 500) at $1.25/tick is the safest starting point. A 20-tick stop costs $25. MNQ at $0.50/tick is a solid second choice for beginners who want more directional movement from the Nasdaq. Both trade over 1 million contracts daily during US hours with tight spreads.

Which futures contracts are most liquid?

ES averages over 1.5 million contracts daily, making it the most liquid futures contract globally. MES exceeds 2 million. NQ, CL, and ZN round out the top five most liquid contracts as of June 2026. Higher liquidity means tighter spreads and cleaner fills on entries and exits.

How much money do I need to start trading futures?

Through a prop firm, you need only the evaluation fee, typically $100-$250 for a $50K account. Apex Trader Funding, Lucid Trading, and MyFundedFutures all offer evaluation accounts in that range. On a personal brokerage account, day trade margins start at $50 for MES and go up to $5,000+ for CL or GC.

What is the best futures contract for scalping?

ES. The liquidity is unmatched, spreads stay at one tick during RTH, and the book is deep enough to handle 5-10 contracts without slippage. NQ is a strong second for scalpers, but the wider point range per bar requires tighter risk management.

Can I trade crude oil futures on a prop firm account?

Some firms allow CL, but many restrict it or cap it at 1-2 contracts regardless of account size. Top One Futures and Bulenox allow CL with position limits. Micro Crude Oil (MCL) is often still permitted even when full-size CL is blocked. Check each firm's allowed instruments list before buying an evaluation, because rules change.

What is the difference between E-mini and Micro E-mini futures?

Micro E-mini contracts are exactly one-tenth the size of their E-mini equivalents. MES is $1.25/tick versus $12.50/tick for ES. MNQ is $0.50/tick versus $5.00/tick for NQ. Same chart, same price action, same underlying index. Micros exist for traders who need smaller position sizing or want to scale in gradually.

What are the best futures contracts to trade overnight?

ES and NQ have the best overnight liquidity among futures, with spreads typically staying within 1-2 ticks during globex (6:00 PM to 9:30 AM ET). GC is active during London hours (3:00-8:00 AM ET). CL has overnight volume but gaps on geopolitical news. All contracts carry wider spreads and lower volume compared to the US session.

Which contract has the highest daily dollar range?

CL averages $1,500-$3,000 per contract per day in dollar terms. NQ produces $1,250-$2,000 per contract daily (250-400 points at $5/tick). GC can range $1,500-$3,500 on active days. Higher range means more profit potential and more risk per position.