Quick Answer, Micro Futures Trading

- MES ticks at $1.25, MNQ at $0.50, MGC at $1.00. Ten micros equal one standard contract in exposure.

- As of June 2026, every major futures prop firm supports micro contracts: Apex Trader Funding, Lucid Trading, MyFundedFutures, Bulenox, TradeDay, Take Profit Trader, Tradeify, and Top One Futures.

- On a 50K prop account with $2,500 EOD Trailing drawdown, the drawdown math makes ES nearly untradeable at normal risk parameters. MES solves that.

- Prop firms almost always count micros 1-for-1 against contract limits (one MES = one contract, same as one ES).

- Don't treat micros as practice. Five MNQ contracts move $2.50/tick combined. Risk management applies exactly the same as with standard contracts.

---

What Micro Futures Actually Are

CME Group launched the first micro equity index futures in May 2019: MES and MNQ. By 2020 the micro suite had expanded to include MYM, MGC, and MCL. Each micro contract represents exactly 1/10th the notional value of its standard counterpart.

Price movement is identical. If ES moves 10 points, MES moves 10 points. The difference is your P&L per point: ES pays $50 per point, MES pays $5. On a 40-point ES move you'd make or lose $2,000 per contract. On MES, that same 40-point move is $200.

This 10:1 ratio holds across all CME micro products. Ten MES contracts have the exact same market exposure as one ES contract. No hidden performance gap, no liquidity penalty at retail size. Same underlying, same price feed, different contract size.

For prop traders, this created something that didn't exist before 2019: the ability to size positions in increments that actually fit inside an evaluation's drawdown buffer.

---

Complete Micro Futures Contract Specs

| Ticker | Contract | Standard Equiv | Tick Size | Tick Value | Point Value | Approx Notional | Typical Prop Margin |

|---|---|---|---|---|---|---|---|

| MES | Micro E-mini S&P 500 | ES | 0.25 pts | $1.25 | $5.00 | ~$27,500 | $40-$100 |

| MNQ | Micro E-mini Nasdaq 100 | NQ | 0.25 pts | $0.50 | $2.00 | ~$40,000 | $50-$150 |

| MYM | Micro E-mini Dow | YM | 1 pt | $0.50 | $0.50 | ~$21,000 | $30-$80 |

| MGC | Micro Gold | GC | $0.10/oz | $1.00 | $10.00 | ~$29,500 | $50-$200 |

| MCL | Micro WTI Crude Oil | CL | $0.01/bbl | $1.00 | $100.00 | ~$7,000 | $50-$150 |

Key differences across the five contracts:

MES has the lowest tick value, making it the most forgiving instrument for new prop traders. It's also the highest-volume micro by a wide margin during US market hours.

MNQ at $0.50/tick sounds cheap, but NQ regularly moves 200-400 points per session. Ten MNQ contracts on a 300-point NQ day generates $600 in P&L range. That adds up.

MCL's point value is unusual: $100 per point on $0.01 tick increments. The tick value is $1.00, but the point (100 ticks) is worth $100. Crude oil moves 1-3 points on a quiet day. Position sizing feels different from the equity index micros.

---

Why Prop Evaluations Are Where Micros Matter Most

The goal in an evaluation isn't maximum profit. It's hitting the profit target while never touching the drawdown floor. Micros serve that goal better than standard contracts on any account under about $150K.

The Drawdown Math

Here's the formula most prop traders ignore:

Max contracts = (Dollar risk per trade) / (Stop loss ticks × Tick value)

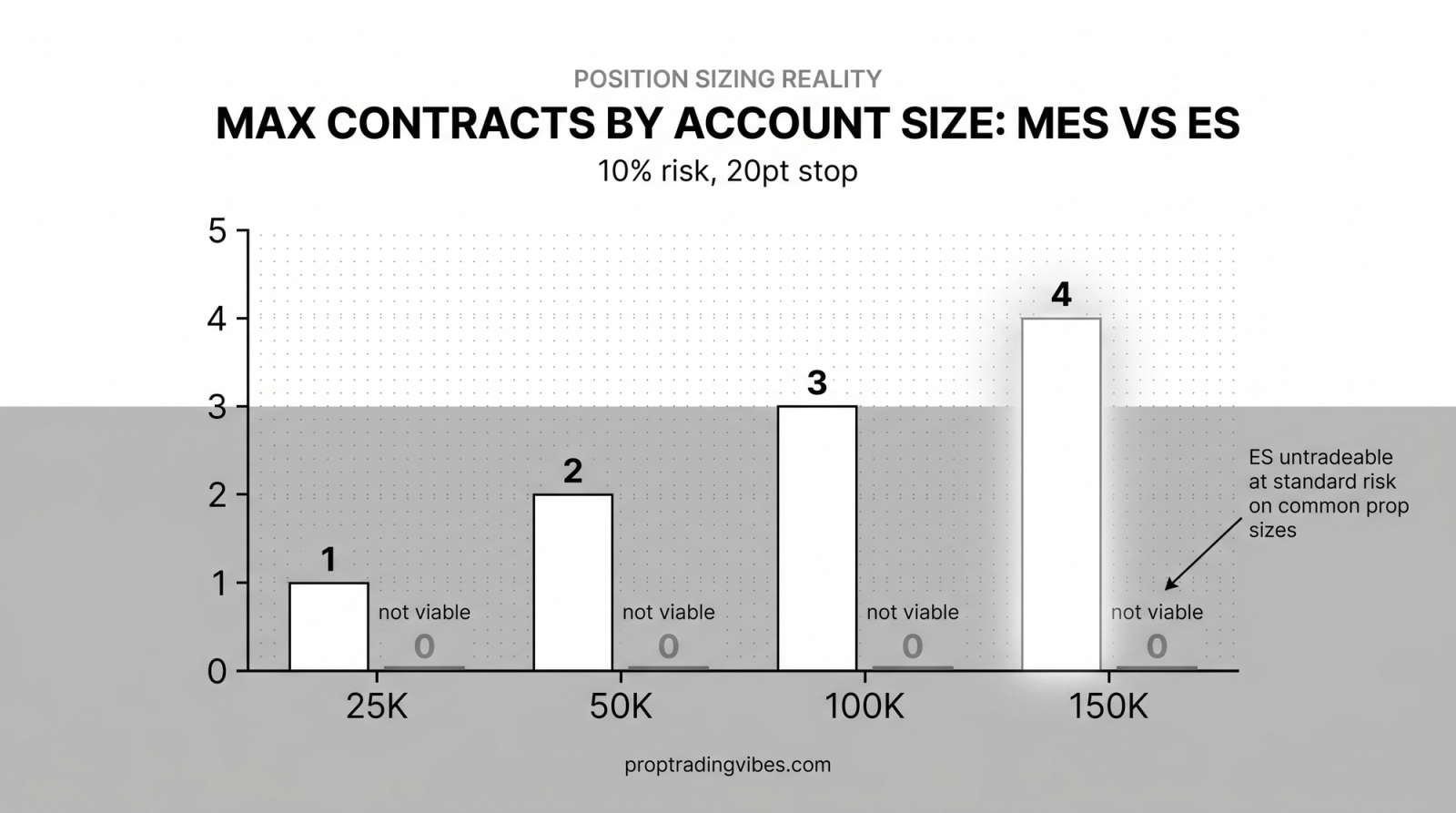

Run it on a 50K account with $2,500 EOD Trailing drawdown, risking 10% of that drawdown per trade ($250), with a 20-point stop:

- MES: $250 / (80 ticks × $1.25) = 2 contracts

- ES: $250 / (80 ticks × $12.50) = 0.25 contracts (can't trade even one)

At 10% risk per trade with a 20-point stop, ES is mathematically unavailable on a 50K account. That's not an opinion. That's arithmetic.

| Account Size | EOD Trailing DD | 10% Risk/Trade | Max MES (20pt stop) | Max ES (20pt stop) |

|---|---|---|---|---|

| 25K | $1,500 | $150 | 1 contract | Not viable |

| 50K | $2,500 | $250 | 2 contracts | Not viable |

| 100K | $3,000 | $300 | 3 contracts | Not viable |

| 150K | $4,500 | $450 | 4 contracts | Not viable |

Even at 20% risk per trade, ES only becomes viable on 100K+ accounts. Micros aren't a beginner option. They're the correct tool for the account sizes most prop traders actually use.

Building a Profit Buffer Progressively

The approach that works: start small, grow into size as the buffer builds.

- Opening phase: 2-3 MES contracts, risk under $150/trade

- Buffer at $500+: increase to 5-6 MES or bring in MNQ

- Buffer at $1,500+: consider adding one standard contract or heavier micro positioning

This turns the evaluation into a progression, not a coin flip. You're never one trade away from failure when early positions are sized to match your actual drawdown tolerance rather than your confidence level.

The Psychological Angle

When a tick is worth $12.50 (ES), every candle feels loaded. When a tick is worth $1.25 (MES), you can focus on execution. Micros don't eliminate the psychological pressure of prop trading, but reducing tick weight reduces the emotional charge of each individual bar. That matters when overtrading and revenge trading are the two most common ways evaluations blow up.

---

How Prop Firms Handle Micro Contracts

As of June 2026, every major futures prop firm supports MES, MNQ, MYM, MGC, and MCL. The main names: Apex Trader Funding, Lucid Trading, MyFundedFutures, Bulenox, TradeDay, Take Profit Trader, Tradeify, Top One Futures, and Breakout. This list covers the firms with verified micro support as of this writing.

Contract Counting Rules

Most firms apply a 1-for-1 count: one MES uses one contract slot, same as one ES. A firm offering 10 contracts on a 50K account lets you hold 10 MES, or 10 ES, or any combination summing to 10.

This creates a tradeoff. Using 10 MES contracts gives you the notional equivalent of one ES contract while using all 10 of your slots. If you want to mix micros and standards, you're working within the same contract ceiling. Know your firm's limit before you combine instruments.

A smaller number of firms offer separate micro and standard contract limits. Check the specific terms for your account tier before assuming this applies to you.

---

Ranking the Five Micro Markets for Prop Trading

Not all micro contracts fit every prop strategy. Here's how they stack up in practice.

MES: The Baseline

Highest micro volume, tightest spreads during CME trading hours, well-defined technical levels. MES is the starting point for most prop traders building a micro-based approach. You can backtest on ES data and run MES execution with nearly identical results.

The limitation: at $5 per point, MES generates slower profit accumulation than MNQ. On accounts with 30-day evaluation windows, that sometimes pushes traders toward MNQ for faster target achievement.

MNQ: More Move Per Contract

NQ moves 200-400 points on a normal session. MNQ at $2 per point means 200 NQ points = $400 per contract. That's significantly more P&L range per contract than MES on most days.

The tradeoff is volatility. Nasdaq can whipsaw hard, particularly around tech earnings, macro data, or large-cap gaps. MNQ rewards strategies that handle that volatility, and punishes those that don't. If your system manages wider ranges well, MNQ produces results faster than MES on most accounts.

MGC: Gold Traders' Micro

MGC at $1/tick (on $0.10 increments) is the correct instrument for futures prop traders who focus on gold. The full GC contract ticks at $10, which creates brutal risk on any account with a tight drawdown. MGC at $1/tick makes genuine gold position trading viable on 50K-100K prop accounts.

See the separate gold futures trading guide for entry setup and session timing. The short version for prop accounts: stick to London and New York sessions, where MGC spreads are tightest. Off-hours spreads on MGC can widen to 2-3 ticks.

MYM: The Overlooked One

MYM ticks at $0.50 with a 1-point tick size. It trades cleanly with decent volume. Most prop traders overlook it in favor of MES or MNQ, but MYM serves two specific purposes: trading when the Dow shows independent behavior from the S&P and Nasdaq, and partial hedging against long MES positions when index correlation breaks.

Volume is lower than MES and MNQ, so keep position sizes reasonable and watch fills during fast moves.

MCL: Use with a Catalyst Only

Crude oil is news-driven. OPEC decisions, EIA inventory reports (Wednesdays, 10:30 AM ET), and geopolitical events can move crude 2-3 points in minutes. MCL handles those moves at $1/tick ($100/point), which is manageable, but the daily range is 2-3x what equity index micros typically produce.

MCL works on prop accounts when you have a specific catalyst and a well-defined technical level. Using it as a daily trading instrument without a directional thesis tends to produce erratic results.

---

Strategies Built Around Micro Contract Sizing

The reduced tick value opens strategies that aren't practical with standard contracts.

Scale-In Entry

Enter 1 MES contract at your initial level. Add 1 more if price confirms by moving 5 points in your favor. Add the remaining position once the trade is clearly working.

If the initial entry is wrong, you lose on 1 contract. If you're right, you've got a full position for most of the move. This is impossible to execute cleanly with 1 ES contract: you're either in or you're not. Micros give you the incremental entry that changes risk profile without changing the underlying thesis.

Bracket Entries

Set two entry prices: first at your primary level, second slightly deeper. Use 2-3 MES at each level. If price hits the first level and reverses, you profit on the first batch. If it drops to the second, your average entry improves and total position grows.

Maximum risk stays defined throughout. You've pre-committed both entry levels and total size before the trade starts.

Multi-Market Spread

On accounts with generous contract limits, spread 10 contracts across 3-4 instruments: 3 MES + 3 MNQ + 2 MGC + 2 MCL, for example. A bad trade in one market doesn't necessarily mean a bad session. You're diversified across equity indices, gold, and crude.

This requires monitoring multiple charts and understanding the correlation between instruments. Not suitable for traders early in their prop career. On 100K+ accounts where contract limits allow it, the diversification effect is real.

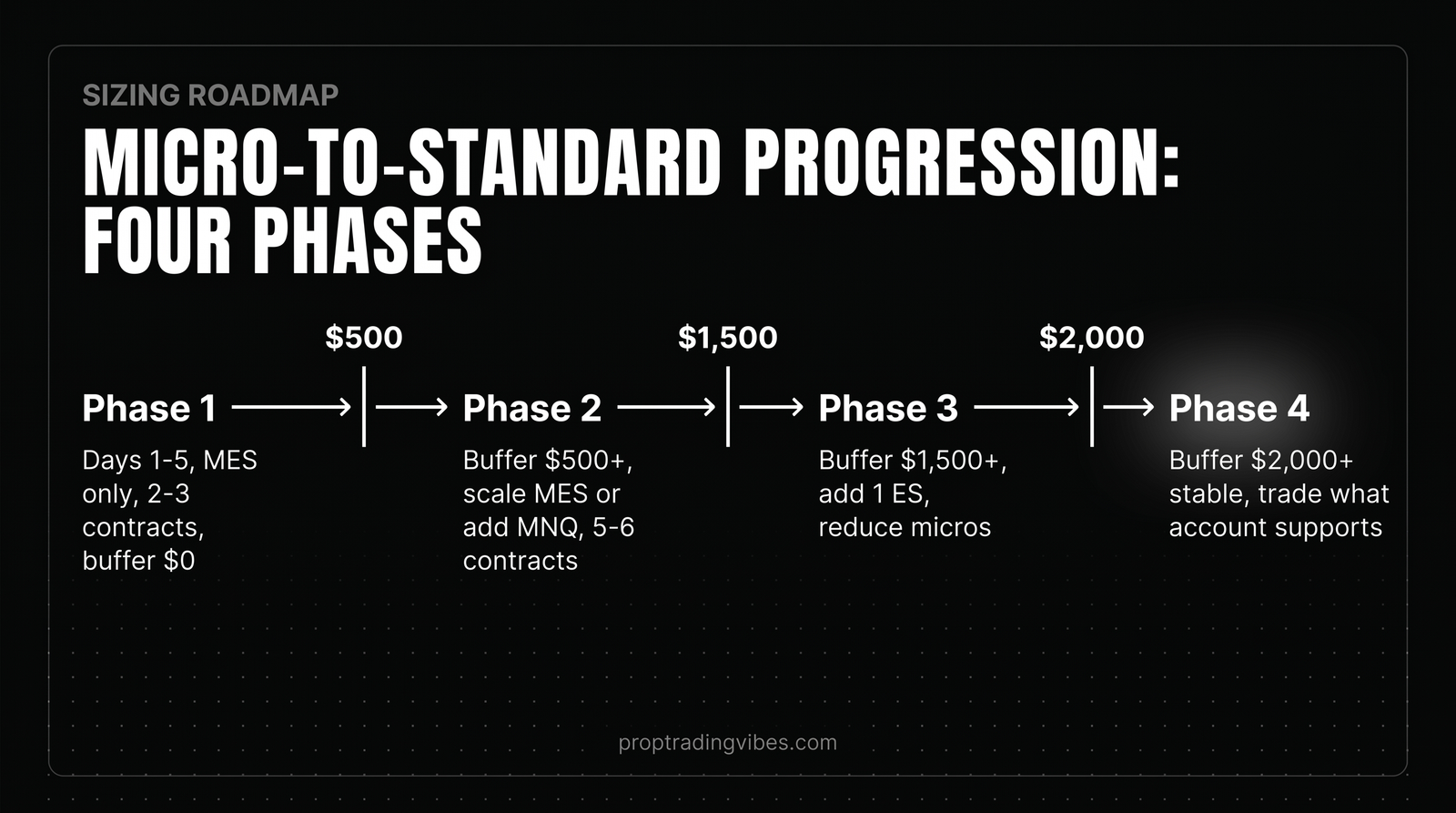

Micro-to-Standard Progression

Start every new prop account with micros only. Build the buffer. Graduate to standard contracts when the math supports it.

- Phase 1 (Days 1-5): MES only, 2-3 contracts

- Phase 2 (Buffer $500+): scale MES or add MNQ

- Phase 3 (Buffer $1,500+): consider 1 ES alongside reduced micro count

- Phase 4 (Funded, buffer stable): trade whatever the account supports

This isn't exciting. It produces no screenshots that look impressive in a Discord server. It does keep you in evaluations long enough to pass them consistently.

---

The Spread Cost You Don't Account For

Micros carry a spread cost that compounds on active traders.

MES and ES both typically trade at a 1-tick spread (0.25 points) during peak hours. In absolute dollars, $1.25 per MES contract vs $12.50 per ES contract. To match one ES contract's exposure you pay $12.50 total in spread on 10 MES, the same.

But on a round-trip commission basis, micros cost more per unit of exposure. If a firm charges $1.50/side per contract, one round trip on 10 MES costs $30. One round trip on 1 ES costs $3.00. Active traders executing 10-15 round trips per day on a micro-heavy book pay materially more in commissions per dollar of P&L than standard contract traders.

The fix: wider targets. Scalping 5-10 ticks on MES during tight market hours is fine. Scalping 5-10 ticks on MGC during off-hours is expensive: a 3-tick spread on a 10-tick target means you're giving up 30% of the move in friction.

Minimum recommended targets by instrument:

- MES: 30-80 ticks (7.5-20 points)

- MNQ: 100-200 points

- MGC: 50+ ticks (5+ dollars per ounce)

- MCL: 20+ ticks (0.20+ per barrel)

At those targets, spread and commission costs stop being a meaningful drag on returns.

---

When to Switch from Micros to Standard Contracts

The switch should be driven by your profit buffer, not your confidence or your newly funded status.

A common mistake: pass the evaluation on micros, get funded, immediately trade full-size ES. The jump from $250 risk per trade to $2,500 risk per trade overnight produces predictable results. The market doesn't care that you just passed.

A safe switching framework:

- Continue trading micros until the funded account has built at least $1,500-$2,000 above the drawdown floor

- Add one standard contract while reducing micro count by the equivalent exposure (e.g., replace 5 MES with 1 MES + 0.5 ES equivalent, meaning reduce to 5 MES and add 1 ES to test)

- Run 5-10 trades at the new size

- If the buffer drops below $1,000 above the floor, return to micros only

The traders who blow funded accounts switch size based on how they feel after a good run. The traders who stay funded switch size based on what the account balance actually supports.

---

Frequently Asked Questions

What are micro futures contracts and how do they differ from standard contracts?

Micro futures are CME-listed contracts sized at exactly 1/10th of their standard counterpart. MES has a $1.25 tick value vs ES at $12.50/tick; MNQ ticks at $0.50 vs NQ at $5.00. Price movement is identical between micro and standard, only the dollar value per tick differs. Ten micro contracts produce the same P&L as one standard contract.

Which micro futures contracts can I trade on a prop firm account?

The five main micros are MES (Micro E-mini S&P 500), MNQ (Micro E-mini Nasdaq 100), MYM (Micro E-mini Dow), MGC (Micro Gold), and MCL (Micro WTI Crude Oil). As of June 2026, all five are supported by Apex Trader Funding, Lucid Trading, MyFundedFutures, Bulenox, TradeDay, Take Profit Trader, Tradeify, and Top One Futures, among others.

How does MNQ's tick value affect prop trading strategies?

MNQ ticks at $0.50 per 0.25-point increment, so each full point is worth $2.00. The Nasdaq 100 typically moves 200-400 points per session, giving each MNQ contract a daily P&L range of $400-$800. That range makes MNQ one of the faster instruments for hitting evaluation profit targets, but the wider daily swings also require wider stop losses than MES.

How do prop firms count micro futures against position limits?

Nearly all prop firms count micro contracts 1-for-1 against your contract limit: one MES uses the same slot as one ES. A 10-contract limit means 10 MES or 10 ES or any mix summing to 10. Some firms are beginning to offer separate micro limits, but this remains uncommon as of June 2026. Verify your firm's specific terms before building a micro-heavy strategy that depends on high contract counts.

What is the correct way to calculate position size for micro futures on a prop account?

Divide your per-trade dollar risk by the product of your stop loss in ticks times the tick value. Example: 50K account, $2,500 EOD Trailing drawdown, risking 10% per trade ($250), 20-point stop on MES: $250 / (80 ticks × $1.25) = 2 contracts. Always round down. Your drawdown buffer is the binding constraint, not your profit target or confidence level.

Are micro futures liquid enough for day trading strategies?

MES and MNQ have strong liquidity during US equity hours with 1-tick spreads and sufficient depth for retail-sized orders. MYM, MGC, and MCL have lower volume and occasionally wider spreads outside peak sessions. For most prop trading purposes the liquidity is adequate. Large micro positions (20+ contracts on a single instrument) may see partial fills on fast moves, but most prop accounts don't reach that size.

What drawdown type applies to most micro futures prop accounts?

Most futures prop firms use EOD Trailing drawdown on evaluation accounts, where the high-water mark moves up with your account balance at end of day and never comes back down. Some firms use Intraday Trailing drawdown, where the trail moves on intraday highs. A smaller number use Static drawdown, which never moves. The drawdown type matters for micro sizing because EOD Trailing locks in a moving floor, which changes your buffer math as you profit.

Should I switch to standard contracts after getting funded?

Not immediately. Continue trading micros until the funded account has at least $1,500-$2,000 in profit above the drawdown floor. Then test one standard contract alongside a reduced micro position for 5-10 trades before fully committing to standard sizing. If the buffer shrinks back toward the floor, return to micros. Size decisions based on account math, not on the feeling that funding means you can trade bigger.